Families often worry about how to provide financial support for a loved one with disabilities without jeopardizing eligibility for Medicaid, Supplemental Security Income (SSI), housing assistance, or other public benefits.

In this interview, elder law attorney Harry Margolis, author of “Get Your Ducks in a Row,” explains the different types of special needs trusts, how they work, when they should be used, and why choosing the right trustee may be one of the most important decisions families make.

Below is a transcript of the interview with Margolis, edited for brevity and clarity.

What special needs trusts are designed to do

Robert Powell: We’ve mentioned special needs trusts in previous videos, but maybe it’s time to take a deeper look at what they are, who should use them and how they work.

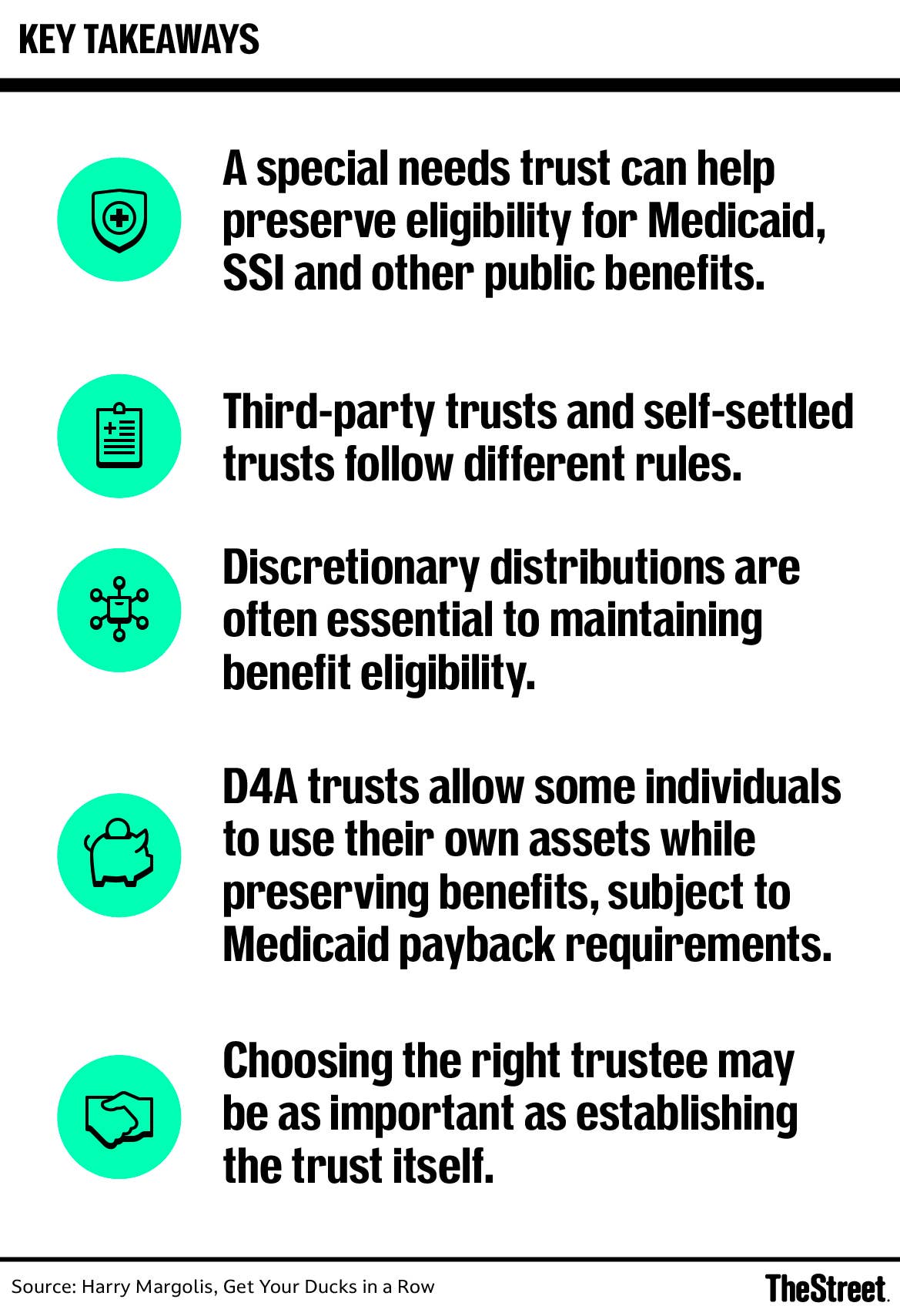

Harry Margolis: A special needs trust is set up so the beneficiary can still qualify for public benefits, whether that’s Medicaid, Supplemental Security Income, public housing, or other programs. The assets in the trust generally won’t be counted when determining eligibility, but the beneficiary can still receive the benefit of those funds.

That can be very important. If you have a child with special needs and want to leave part of your estate to that child, leaving assets outright could cause the loss of benefits. In some cases, that can be catastrophic.

Depending on the disability, the beneficiary also may not be able to manage the funds. A trust can be an effective vehicle for managing money on their behalf.

People can also become disabled later in life and need public benefits programs to help pay for services such as personal care attendants at home. If they own assets outright, they may not qualify for Medicaid assistance.

The two main types of special needs trusts

Harry Margolis: There are essentially two kinds of special needs trusts.

One is a self-settled trust, which is created with the beneficiary’s own assets. The other is a third-party trust, which is created and funded by someone else, such as a parent or grandparent.

The rules are very different for the two types.

How third-party special needs trusts work

Harry Margolis: Let’s start with a third-party trust.

This is a trust created by a parent or grandparent using their own money. The rules are relatively flexible. The trust can benefit one person during their lifetime and then pass assets to other beneficiaries later. It can even benefit multiple people.

The main rule is that the beneficiary should not serve as trustee. The beneficiary should not be managing the funds.

In addition, distributions must be discretionary. If Medicaid or another agency can argue that the trust is required to pay for certain expenses, such as health care or housing, the assets may become countable for benefit purposes.

The trust should clearly state that the trustee has discretion to make distributions or not make them and may pay funds directly to the beneficiary or on the beneficiary’s behalf.

The key concept is discretion.

How self-settled special needs trusts work

Harry Margolis: Traditionally, if someone created a trust for their own benefit and had access to the assets, those funds would be considered available when determining eligibility for benefits.

Congress created a safe harbor often referred to as a D4A trust, sometimes called a payback trust.

Under these rules, an individual can create a trust for their own benefit using their own assets if they are under age 65 when the trust is established and if the trust includes a Medicaid payback provision.

The provision states that when the beneficiary dies, any assets remaining in the trust must first reimburse the state Medicaid agency for benefits provided during the beneficiary’s lifetime.

That is often a reasonable tradeoff. The individual can receive Medicaid, SSI, subsidized housing, food assistance, and other public benefits during life. If assets remain at death, they are subject to reimbursement claims.

Why trustee selection matters

Harry Margolis: Both types of trusts can be very effective planning tools.

One of the biggest challenges is selecting the right trustee. It could be a sibling, a parent, a trust company, a bank, or another professional.

Finding the right fit can be difficult, but it is one of the most important decisions families make.

When a pooled trust may be the answer

Harry Margolis: There’s also a third option known as a D4C trust, often called a pooled trust.

Congress authorized nonprofit organizations to administer special needs trusts for multiple beneficiaries. While each beneficiary has a separate account, the organization serves as trustee and manages the administration.

These organizations typically have extensive experience working with individuals with disabilities and understand the public benefits system.

Families give up some control because a nonprofit serves as trustee, but they gain professional administration and expertise.

For smaller trusts, a pooled trust often solves the question of who should serve as trustee.

Many pooled trusts can also act as trustees for third-party special needs trusts created by parents or grandparents.

The case for co-trustees

Robert Powell: Is there ever a situation where co-trustees make sense?

Harry Margolis: Absolutely.

I like co-trustees because the family member knows the beneficiary best, while a professional trustee can handle accounting, taxes, and compliance with public-benefit rules.

It’s a good hybrid solution. It also gives the family member someone to point to when denying an inappropriate request.

Sometimes the professional trustee can be the one who says no.

Can a trust be funded later?

Robert Powell: Does the trust have to be funded immediately, or can it be funded after the grantor dies?

Harry Margolis: Many third-party special needs trusts are funded only after the parent’s death.

Parents often use their own assets to support a child during their lifetime. When they die, the trust serves as the vehicle that receives the inheritance.

That approach avoids disinheriting the child while also preventing assets from passing outright and jeopardizing benefits.

Related: ABLE accounts open new options for people with disabilities