Investors should expect a leaner, quieterFederal Reserve coming up very soon.

That’s Morgan Stanley’s forecast for Kevin Warsh’s debut as Chair of the Federal Reserve which includes a warning to Wall Street about the central bank’s near-term rate path and long-term communications style.

Morgan Stanley said when Warsh takes the podium for his first post-meeting press conference at the Federal Open Market Committee June 17, Fed watchers will notice a sharp change in tone from that of his predecessor Jerome Powell.

Warsh has been highly critical of forward guidance and economic forecasting tools like the Summary of Economic Projections or “dot plot” that investors have come to rely upon.

He could very likely refuse to answer questions from the media about his stated desires for a “regime change” that includes scaled-back communications and a smaller balance sheet.

“We would also not be surprised if he declines to answer certain questions, particularly those about the expected future path of policy. If Chair Warsh is serious in his belief that the Fed talks too much and forward guidance injects as much volatility as it removes, then he may choose to limit his forward-looking remarks,’’ according to the June 12 note emailed to TheStreet.

That could include a significant scaling back of future policy hints and a reduced number of media briefings, the note said.

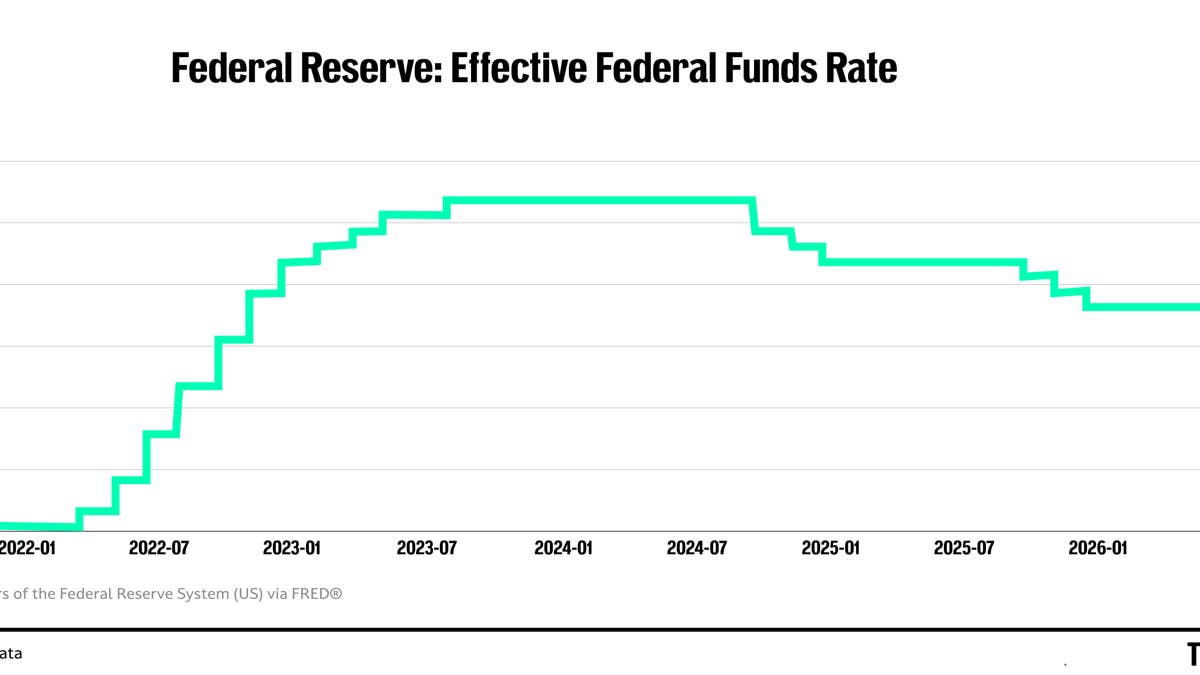

Fed keeps rates steady thus far this year

The FOMC continued to hold the benchmark Federal Funds Rate steady at 3.50% – 3.75% at its April 30 meeting, Powell’s last as Chair. He remains on the Board of Governors until April 2028.

Policymakers had cut rates by 25 basis points at its last three meetings of 2025 to shore up the softening labor market.

These “insurance” cuts stopped after the majority of policymakers decided the risk from higher prices was outweighing signs that the jobs market was stabilizing.

The funds rate influences the cost of short-term borrowing from credit cards to student loans and also can impact mortgage rates.

FRED Economic Data/TheStreet

Fed’s dual mandate requires a tricky balance

The Fed’s dual mandate from Congress requires maximum employment and stable prices.

- Lower interest rates support hiring but can fuel inflation. This risks fueling further inflation, potentially leading to an inflationary spiral.

- Higher rates cool prices but can weaken the job market. This increases the cost of borrowing and further stifles economic activity.

Historically, the U.S. central bank has favored stable jobs over higher prices. Inflation has been running above the Fed’s 2% annual target for the past five years.

Morgan Stanley’s Fed rate-cut forecast

Along with stricter inflation discipline, the June 17 post-meeting official policy statement likely will remove the language about longstanding easing bias in favor of more neutral guidance.

Initial expectations, especially those of President Donald Trump, were that the new Chair would lean dovishly toward rate cuts when the president nominated Warsh in January.

But the volatile energy prices from the monthslong Iran War leaves the 12-member FOMC with zero room to maneuver interest rates.

Related: Bond traders drastically shift Fed rate-hike bets

Hence Morgan Stanley expects rates to remain firmly on hold for the foreseeable future, with one 25 basis points-rate cut in 2027.

“We think (Warsh)…will acknowledge the risk of persistent inflationary pressures from higher energy prices but speak optimistically about AI-related uncertainties,” the note said.

Press conferences key to Warsh’s new strategy?

Among other uncertainties, the note said that information on the number of press conferences could impact front-end pricing the most.

The transition from four post-meeting press conferences a year to eight occurred in January 2019 under Powell, in part because FOMC participants did not want investors to believe that the Fed held up a higher bar to change policy at meetings without one.

Before that change took place, markets often worried that they lacked an immediate public platform that would explain sudden shifts in monetary policy.

“If the Fed reverted to a press conference once per quarter, investors might rethink whether the Fed might hike rates in July or October this year, or January or April next year,’’ Morgan Stanley said.

As I reported, nervous bond traders had been drastically upping the ante on a Fed rate hike since early May as the war dragged on, oil prices surged and consumer prices continued to spike.

Futures traders lowered their expectations June 15 of an increase in the benchmark Federal Funds Rate in December of this year to near 90% probability to almost 60%, according to the widely watched CME Group FedWatch Tool, after the Iran peace agreement was announced.

Related: Warsh’s first Fed meeting resets interest rate-cut bets