Not only has the Iran War driven up energy costs for Americans, but higher prices — not all related to oil — for many goods and services are erasing our desperately needed wage gains.

Federal Reserve Bank of Chicago President Austan Goolsbee has had enough.

He said he remains concerned aboutinflation and questioned whether all the factors driving prices up are temporary shocks to the economy,

“We’ve been dealing with an inflation problem that’s well above the target and has been going the wrong way,” Goolsbee said June 22 in an interview on American Public Media’s Marketplace radio program.

With the labor market stable, he is focused on figuring out whether too-high inflation will persist or recede as the effects of high tariffs fade and the conflict in the Middle East is resolved, Reuters reported.

What makes Goolsbee’s comments notable is less the content and more the fact that he expressed them.

Fed Chair Kevin Warsh has begun a massive reform of the U.S. central bank’s communications, and one key tenet of the overhaul is to significantly curb speeches and statements from his fellow 18 Fed officials.

Under former Chair Jerome Powell, the Fed regional bank presidents, including the FOMC voting members, have been more vocal in recent months about inflation than the labor market. Goolsbee is not a voting member of the policymaking panel this year.

But it does appear, at least to this reporter, that the muzzles have been deployed.

Warsh calls for “regime change” at Fed

Warsh testified repeatedly during his Senate nomination hearing April 21 that he would maintain Fed independence from executive authority.

He also called for a “regime change” at the central bank that includes:

- Dropping the quarterly “dot plot” which shows Federal Open Market Committee member expectations for short-, intermediate- and long-term economic projections.

- Fewer press conferences and speeches by FOMC officials on economic conditions and interest-rate outlooks.

Warsh’s new communications era kicks off

At the June 17 post-Federal Open Market Committee meeting press conference, Warsh’s biggest announcement was the formation of five task forces of outside consultants supported by Fed staff that will study current processes and make strategic recommendations for state-of-the-art updates.

One of the task forces will focus on communications, including the longstanding practice of Fed officials, especially the 12 regional bank presidents, to discuss economic issues and their forecasts not only with their geographic constituents but also with the financial press.

Warsh has made clear for years that he is not a fan of this mode of communications, and frankly would prefer his Fed colleagues to put a sock in it.

The new crickets were very noticeable after the June 16-17 meeting, when, instead of coast-to-coast comments on interest rates, statement language, labor markets, and inflation, there was relative silence.

The June post-FOMC statement also dropped all language about forward guidance, which had indicated to markets whether policymakers were tilting toward a rate hike, cut, or hold.

Tony Welch, Chief Investment Officer at SignatureFD, told TheStreet in an email that under Warsh’s new era, the Fed may increasingly ask markets to respond to data as it arrives rather than tell markets what to expect.

The bottom line, Welch said, was “the new Fed appears focused on flexibility and inflation credibility, not on guiding markets toward a predetermined path for interest rates.”

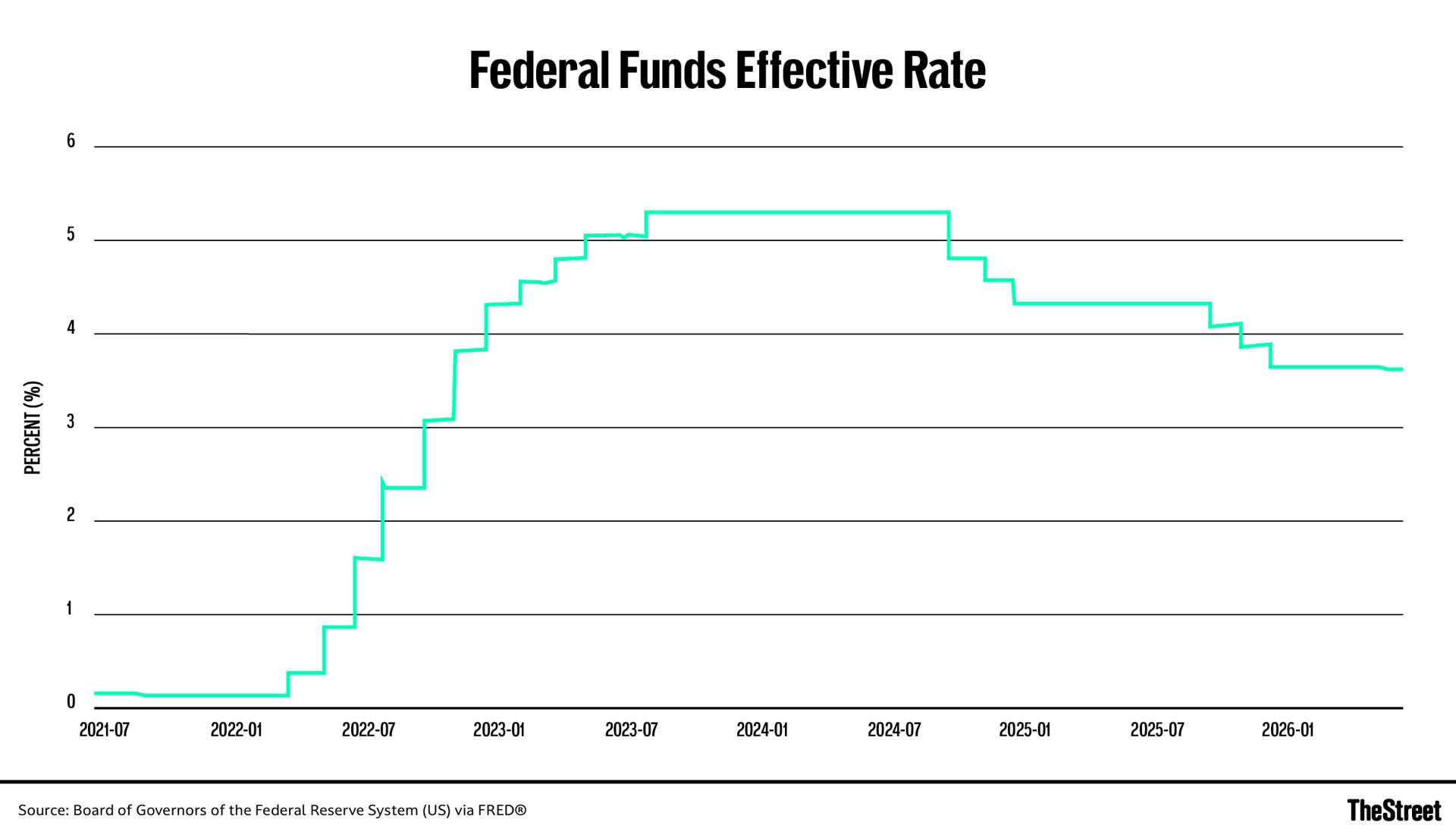

Fed keeps rates steady thus far this year

The FOMC voted 12-0 June 17 to hold the benchmark Federal Funds Rate steady at 3.50% to 3.75%.

Policymakers had cut rates by 25 basis points at its last three meetings of 2025 to shore up the softening labor market.

These “insurance” cuts stopped after the majority of policymakers decided the risk from higher prices was outweighing signs that the jobs market was stabilizing.

The funds rate is the interest rate at which banks lend balances at the Federal Reserve to other banks overnight.

Changes in the funds rate trigger a chain of events that affect:

- Other short-term interest rates.

- Foreign-exchange rates.

- Long-term interest rates.

- The amount of money and credit in the economy.

- And ultimately, a range of economic variables, including employment, output, and prices of goods and services.

Fed’s dual mandate requires a tricky balance

The Fed’s dual mandate from Congress requires maximum employment and stable prices.

- Lower interest rates support hiring but can fuel inflation. This risks fueling further inflation, potentially leading to an inflationary spiral.

- Higher rates cool prices but can weaken the job market. This increases the cost of borrowing and further stifles economic activity.

The widely-watched CME Group FedWatch Tool currently points to the December FOMC meeting as the most likely venue for the central bank’s first rate hike of the year.

Related: Fed’s Warsh leaves markets guessing on rate hikes

Futures traders are penciling in an approximately 60% probability that the 12-member FOMC will hike rates by at least 25 basis points before year-end.

Other Fed watchers, including Bank of America and Goldman Sachs, expect rate hikes sooner to quell inflation.

Goolsbee expresses concern about inflation risk

The May Personal Consumption Expenditures, the Fed’s current preferred inflation gauge, is due June 25.

- Market consensus for the core PCE Index (year-over-year) sits around 3.3%, matching the April reading, which was the highest annual print in over three years.

- But the Federal Reserve Bank of Cleveland models project as of June 22 that Headline PCE (year-over-year) will come in at 3.97% up from April’s 3.8%.

“What’s been on my mind is, what is the evidence that this is going to be temporary, and that we’re going to get back on path to 2%, which is what we’ve promised,” Goolsbee said, referring to the Fed’s own 2% target of annual inflation.

Goolsbee said he is particularly focused on elevated services inflation, which is not directly related to higher oil prices from the Iran War or higher goods prices from tariffs.

“There are some signs, like the fact that some of the inflation came from tariffs and that’s supposed to be one and done, that we could get some resolution in the Middle East and maybe that inflation would go away,” he said.

“The fact that we’ve seen it in services, which historically is pretty persistent, is a little more disturbing,” he said, according to Reuters.

According to Bloomberg, Goolsbee said that he’s sympathetic to Warsh’s view that the central bank shouldn’t be giving too much guidance on what policymakers are likely to do with interest rates in the future.

Incorrect predictions about the future path of the economy can hurt the Fed’s credibility, Goolsbee said.

Related: Goldman hints at Fed’s next interest-rate bet under Warsh