Higher Affordable Care Act (ACA) premiums are now in effect, and for an estimated 20 million Americans the increase is hitting without the cushion of enhanced federal subsidies.

Congress failed to extend the expanded advance premium tax credits that were introduced during the pandemic.

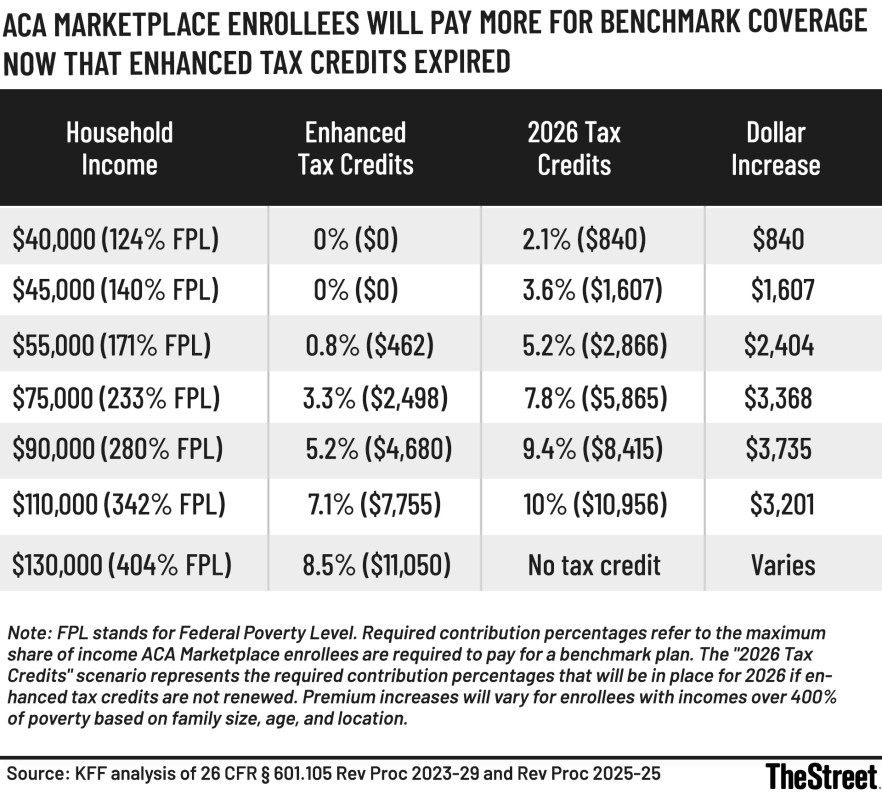

As a result, many consumers are paying sharply higher premiums in 2026, particularly households with income above roughly 150% of the federal poverty level, according to Jae Oh, author of Maximize Your Medicare.

In an interview, Oh noted that health care costs have continued to rise steadily, and without the enhanced subsidies, more families are confronting difficult trade-offs between coverage and affordability.

Below is a transcript of that interview, edited for clarity and brevity.

Robert Powell: It’s the new year, and that means new premium schedules for Affordable Care Act health plans are now in effect. Here to talk about what that means is Jae Oh, author of Maximize Your Medicare. Jae, welcome.

Jae Oh: Thanks for having me, Bob.

Powell: I’m not sure if you’re the bearer of good news or bad news on this one.

Oh: Largely bad news. Congress failed to reach an agreement to extend the enhanced advance premium tax credits. As a result, higher premiums have taken effect without those subsidies.

For households with income above about 150% of the federal poverty level, premiums are higher. How much higher varies by household, location and plan, but the ripple effects are real. Some people are already considering canceling their ACA coverage.

Health insurance has gotten more expensive for millions of Americans.

Health insurance has gotten more expensive for millions of Americans.

KFF analysis

Is dropping coverage a mistake?

Powell: That doesn’t sound like a great move. Is it?

Oh: It depends on the household. Without knowing someone’s full situation, it’s hard to make a blanket statement.

One thing often missing from the debate is the ACA’s out-of-pocket maximum. Even with all the frustrations people have with health insurance, that cap limits total financial exposure. If someone has $300,000 in medical bills in a year, insurance prevents financial ruin.

Insurance isn’t a coupon. It’s protection against catastrophic loss.

That said, for some households, the likelihood of facing that kind of risk may be very low. When families are choosing between food and health insurance premiums, food clearly comes first. This becomes a household-by-household decision.

Short-term and limited coverage options

Oh: There are alternatives people are looking at. Short-term health insurance plans do exist. Some can now be renewed during the year, but they involve underwriting.

Pre-existing conditions may not be covered. If something in your medical history later comes to light, it could be excluded. These plans are not regulated under the same rules as the ACA, and people need to understand that before enrolling.

Downgrading ACA coverage may no longer be an option

Powell: What about staying in the ACA but moving to a lower-tier plan?

Oh: For many people, that window has already closed. Open enrollment is over in most locations. That leaves some households facing a tough choice: keep paying much higher premiums or stop paying and become uninsured.

There are also very limited products available, such as hospital indemnity plans, cancer-specific plans or heart attack plans. These pay a fixed dollar amount if a covered event occurs. They’re essentially Band-Aids for households that cannot afford much higher ACA premiums.

I’m not saying these developments are good or bad. They’re just the reality many families are facing.

Faith-based health sharing plans

Powell: What about faith-based plans?

Oh: Some households have had acceptable experiences with them. But coverage decisions are discretionary. If a claim is denied, you may have little or no recourse.

These plans are not regulated like ACA plans. There’s no state regulator or federal agency overseeing them. My concern is Murphy’s law: people lower their premiums, then discover on the back end that they’re not covered and have nowhere to appeal.

Why this feels worse than before

Powell: To put this in context, the enhanced premium tax credits came out of COVID-era legislation. Before that, they didn’t exist. In a sense, we’re reverting to the pre-COVID structure.

Oh: That’s exactly right. Meanwhile, the underlying cost of health care has continued rising, roughly 6% to 8% a year.

So insurance is now covering much more expensive care, which drives premiums higher. Then the enhanced credits are removed. That’s the double whammy behind today’s headlines.

Planning matters more, not less

Powell: Anything we missed?

Oh: One key takeaway is that health coverage is income-related. The ACA and Medicare both tie premiums to taxable income.

If you’re not paying attention, everything else in your household can stay the same, but suddenly your premiums jump sharply. That’s even more dramatic under the ACA than under Medicare Part B.

This moment highlights the importance of income planning and coordination. Some people may think the answer is to delay retirement or give up. But many households planned for this possibility and can still retire early comfortably.

It’s not all doom and gloom, but it does reinforce the need for careful planning.

Related: Retirement Industry 2026 Legislative and Regulatory Priorities