For Americans considering retirement abroad without leaving the U.S. financial system, Puerto Rico often appears near the top of the list.

The Caribbean island offers tropical weather, a vibrant culture and the familiarity of a U.S. territory. But while Puerto Rico is sometimes described as a tax haven, the reality for retirees is more complicated.

In fact, relocating to Puerto Rico often means navigating two tax systems, understanding investment implications and evaluating whether tax incentives truly apply to retirees.

That’s according to Daniel Gonzalez-Maisonet, CPA/PFS, managing partner at Fulcro Financial in San Juan, who discussed the issue in a recent interview.

Below is a transcript of that interview, edited for clarity and brevity.

Robert Powell: Do you have designs on retiring to Puerto Rico? Here to talk with me about that is Daniel Gonzalez-Maisonet, CPA, PFS, managing partner, financial planner and wealth manager at Fulcro Financial in San Juan, Puerto Rico. Daniel, welcome.

Daniel Gonzalez-Maisonet: Thank you, Robert, for having me.

Robert Powell: It’s a pleasure. Let’s start with this. Why do you think Puerto Rico is an attractive place to retire?

Why Puerto Rico appeals to retirees

Daniel Gonzalez-Maisonet: People considering retirement may be attracted by the idea of relocating to a place that is both a U.S. territory and part of the Caribbean. It offers a mix of familiarity and a new lifestyle, which can be appealing for many retirees.

Is Puerto Rico a tax haven?

Robert Powell: Sometimes people regard Puerto Rico as a tax haven. What does that mean?

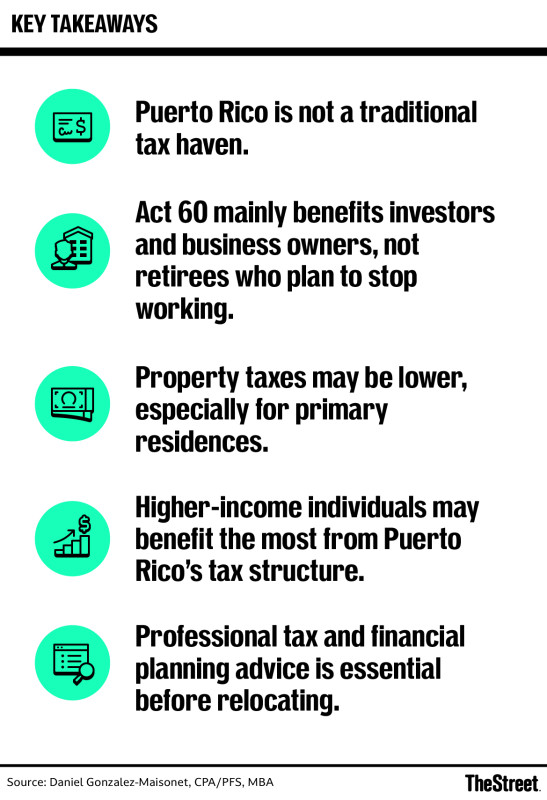

Daniel Gonzalez-Maisonet: I have some reservations about that description. In the traditional offshore sense, Puerto Rico is not really a tax haven. The island operates under a dual tax framework between the U.S. and Puerto Rico, which creates complexity.

Puerto Rico has been working to attract business owners and investors by offering more tax-efficient structures. But those benefits come with economic trade-offs. Individuals relocating to Puerto Rico must understand the compliance requirements that exist under both the Puerto Rico tax code and the U.S. tax code.

Understanding income taxes for retirees

Robert Powell: Let’s talk about what retirees need to know about income taxes in Puerto Rico.

Daniel Gonzalez-Maisonet: If someone from the U.S. mainland relocates to Puerto Rico, they may find themselves dealing with two tax jurisdictions.

For example, a retiree who still has income sources tied to the U.S. could end up filing U.S. tax returns while also taking credits in Puerto Rico. That duality is one of the first issues to understand.

Another important consideration involves investment portfolios. Assets held by retirees may be treated differently depending on whether they are considered located in the United States under the Internal Revenue Code.

Portfolio management becomes especially important because the earnings generated from those assets – dividends, interest and capital gains – can have tax consequences. Retirees need to understand those consequences and plan accordingly.

TheStreet

Potential downsides of Puerto Rico’s tax advantages

Robert Powell: What are some of the downsides to Puerto Rico’s tax advantages?

Daniel Gonzalez-Maisonet: Tax incentives can change over time. For instance, if federal tax changes make it more tax-efficient for U.S. residents to remain on the mainland, the difference between Puerto Rico and the mainland may narrow.

Because of that, taxation alone should not be the main driver for relocating. In our professional framework, we don’t recommend making a life decision like retirement relocation solely because of taxes.

Taxes are one factor, but retirement decisions should consider a broader range of financial and personal factors.

What retirees should know about Act 60

Robert Powell: Puerto Rico has something called Act 60 that retirees should know about.

Daniel Gonzalez-Maisonet: Yes. Act 60is a policy designed to attract investors and business owners to Puerto Rico.

It typically offers a flat tax rate of about 4% for qualifying business activities, along with exemptions on certain Puerto Rico-sourced capital gains.

However, it’s important to understand that Act 60 is generally aimed at people who relocate to Puerto Rico to operate a business or investment activity. It typically requires becoming a Puerto Rico resident and may include requirements such as hiring local employees.

Because of those requirements, Act 60 may not apply to someone who simply retires and does not plan to work or operate a business.

Anyone considering applying for a tax decree should consult with a qualified tax or legal adviser to understand the requirements.

Property taxes and housing considerations

Robert Powell: We often look at the total tax burden, including property taxes. What should retirees know about property taxes in Puerto Rico?

Daniel Gonzalez-Maisonet: Property taxes can be relatively manageable compared with many parts of the mainland United States.

If you relocate to Puerto Rico and your home becomes your primary residence, it can often qualify for a property tax exemption.

Another factor to understand is that Puerto Rico’s property tax system is based on older valuation assessments. Policymakers have discussed the possibility of reforms, but nothing has been finalized yet.

Income and estate tax considerations

Robert Powell: Retirees are often interested in income and estate tax exemptions. What should they know?

Daniel Gonzalez-Maisonet: If someone does not have a tax decree under programs such as Act 60, they will likely still be dealing with the dual U.S.–Puerto Rico tax framework.

For example, a Puerto Rico resident who is a U.S. citizen and whose only income sources are Social Security and income from a Puerto Rico-qualified retirement plan may find those sources potentially tax-free.

However, once other income sources are added – such as distributions from U.S. retirement accounts or investment portfolios – the situation becomes more complicated.

As we often say, income sources can “contaminate” certain areas of the tax code, meaning that different types of income interact across both jurisdictions.

Why professional advice is critical

Robert Powell: Given those complexities, it seems especially important to work with a professional familiar with both tax systems.

Daniel Gonzalez-Maisonet: Absolutely. Ideally, someone should work with a CPA who is also a financial planner.

Before making a decision to relocate, retirees should conduct a planning exercise that evaluates their income sources, financial situation and family structure.

That process can involve running hypothetical scenarios to determine whether relocating makes sense financially before engaging legal or tax advisers to finalize the move.

Who benefits most from relocating to Puerto Rico?

Robert Powell: Is there a particular type of person who benefits most from relocating?

Daniel Gonzalez-Maisonet: Higher-income individuals may see the most benefit.

For example, someone living in high-tax states such as New York or California may still face relatively high tax burdens on the mainland. For those individuals, Puerto Rico could offer greater tax efficiency.

For average earners, however, taxes alone may not provide a significant advantage. Instead, the decision may hinge on other factors such as lifestyle, cost of living and personal preferences.

Lifestyle and quality of life

Robert Powell: We’ve focused on the financial aspects, but Puerto Rico also offers a tropical climate, vibrant culture and great food.

Daniel Gonzalez-Maisonet: Exactly. Taxation should not necessarily be the primary reason someone chooses Puerto Rico.

Depending on personal circumstances, relocating could make sense for lifestyle reasons. The role of advisers is to help determine whether the move also makes sense financially.

Confidence in Puerto Rico’s financial system

Daniel Gonzalez-Maisonet: One final point I’d like to emphasize is that Puerto Rico’s financial system operates under the same regulatory umbrella as the U.S. mainland, including institutions overseen by agencies such as the FDIC, SIPC and the Securities and Exchange Commission.

For retirees who are relocating with their life savings, it’s important to know that their wealth is being managed within a stable and well-regulated financial system.

Closing remarks

Robert Powell: Daniel, thank you for sharing your knowledge. My guest has been Daniel Gonzalez-Maisonet, CPA, PFS, managing partner at Fulcro Financial in San Juan and a member of the American Institute of CPAs’ PFP Champions Task Force.